�������ĵ�������ŦԼ��ѧ����ϵ����Aswath Damodaran���ųơ�������̫������Ŀǰ��NYU����ѧԺ���ڹ�ֵ�γ̣��ǻ����������ŵĽ���֮һ��Ϊ��������ѵ�˴����ľ�Ӣ������������Ҫ�����˴Ӳ�����ʿ�ȫ���Ʊ���ۡ�

����When looking at how stocks are priced and especially when comparing pricing across stocks, we almost invariably look at pricing multiples (PE, EV to EBITDA) rather than absolute prices.

����That is because prices per share are a function of the number of shares and are, in a sense, almost arbitrary. Before you respond with indignation, what I mean to say is that I can make the price per share decrease from $100/share to $10/share, by instituting a ten for one stock split, without changing anything about the company.

����As a consequence, a stock cannot be classified as cheap or expensive based on price per share and you can find Berkshire Hathaway to be under valued at $263,500 per share, while viewing a stock trading at 5 cents per share as hopelessly overvalued.

�����ڿ���Ʊ����ζ���ʱ�������ǶԲ�ͬ��Ʊ�ļ۸���жԱ�ʱ�����Ǽ����ᶼ��ȥ������ָ�꣨PE, EV �� EBITDA����������ȥ�����Լ۸���Ϊ��Ʊ��ÿ�ɼ۸��ɹ�Ʊ������������ij�̶ֳ��ϣ����ǿ���Ͷ���ġ�

�����ȱ�������������ô˵����˼�ǣ�ֻҪ��1ֻ�ɲ�ֳ�10ֻ�ɣ��ɼ۾��ܴ�100�������10����ÿ�ɣ����ǹ�˾����ͬһ�ҡ����ԣ�����������ÿ�ɼ۸�ĸߵ����жϹ�Ʊ�DZ��˻��ǰ�����ᷢ�ֹɼ۸ߴ�263,500����IJ���ϣ������ΤҲ����������Ҳ������ķ��ֽ��۸��5���ֵĹ�ƱҲ���ǻᱻ�߹���

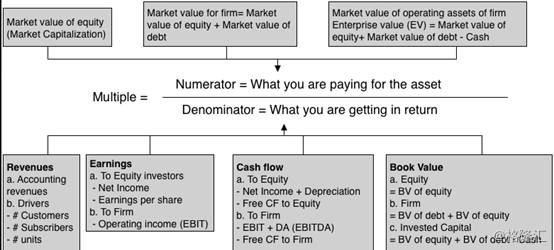

����The process of standardizing prices is straight forward. In the numerator, you need a market measure of value of equity, the entire firm (debt + equity) or the operating assets of the firm (debt + equity -cash = enterprise value). In the denominator, you can scale the market value to revenues, earnings, accounting estimates of value (book value) or cash flows.

�����ü۸�����Ĺ��̺ܼ��ѷ�����Ϊ��˾������Ȩ�桢��������˾����ծ+������Ȩ�棩���г���ֵ��Ҳ�����ǹ�˾�ľ�Ӫ���ʲ���ֵ����ծ+������Ȩ��-�ֽ�=��ҵ��ֵ�����ѷ�ĸ��ΪӪ�գ������룬��ֵ�������ֵ�������ֽ����Ļ�ƹ�ֵ��

����

����ͼƬע�ͣ�

����������Ϊ������Ʊ�۸��Ƿ�������ָ��Ӧ���ǣ���Ϊ��ҵ���ʲ�֧���ļ۸�÷�����õĻر����档���ӿ���Ϊ���������1������ҵ������Ȩ����г���ֵ����ֵ������2����ҵ���г���ֵ��Ҳ����ҵ������Ȩ����г���ֵ+��ծ���г���ֵ����3����ҵ��Ӫ���ʲ����г���ֵ����������Ȩ���г���ֵ+��ծ���г���ֵ-�ֽ� ��ĸ�������������Ӫ�գ������룬�ֽ����������ֵ��

����As you can see, there is a very large number of standardized versions of value that you can calculate for firms, especially if you bring in variants on each individual variable in the denominator.

����With net income, for instance, you can look at income in the last fiscal year (current), the last twelve months (trailing) or the next year (forward). The one simple proposition that you should always follow is to be consistent in your definition of multiple.

����������������ҵ�ļ�ֵ�кܶ�������ļ���汾���������ڷ�ĸ�ĸ���������������ɱ�����ʱ������ˡ����羻������һ����������һ����ľ����������棩��Ҳ�����ǹ�ȥ12���µ����棨�������棩����������һ������棨Ԥ�����棩����Ҫ���ص�һ����ԭ�����������ָ���µĶ����ʼ�ձ���һֱ��

����The "Consistent Multiple" Rule: If your numerator is the market value of equity (market capitalization or price per share), your denominator has to be an equity measure as well (net income or earnings per share, book value of equity.

����For example, a price earnings ratio is consistent, since both the numerator and denominator are equity values, and so is an EV to EBITDA multiple. A Price to EBITDA or a Price to Sales ratio is inconsistent, since the numerator is an equity value and the denominator is to the entire business, and will lead to conclusions that are not merited by the fundamentals.

������ָ��һ���ԡ�ԭ�����������������Ȩ����г���ֵ������ֵ����ÿ�ɹɼۣ�����ĸ�ͱ���Ҳ����������Ȩ��ķ������㣨��������EPS�����ǹ�Ȩ�������ֵ�������磬P/E���ָ����ϡ�һ���ԡ�ԭ����Ϊ���ӡ���ĸ���ǹ�Ȩ��ֵ��EV����ҵ��ֵ����EBITDA�� δ����Ϣ��˰��۾ɼ�̯��ǰ������������ָ�ꡣ�ɼ�/EBITDA�����߹ɼ�/Ӫ�ն��Dz����ϡ�һ���ԡ�ԭ���ָ�꣬��Ϊ����ָ���ǹ�Ȩ��ֵ����ĸ��������ҵ�ģ���ص��½���ͻ����治���ϡ�

����Pricing �C A Global Picture

�����۸�-ȫ��չͼ

����To see how stocks are priced around the world at the start of 2017, I focus on four multiples, the price earnings ratio, the price to book (equity) ratio, the EV/Sales multiple and EV/EBITDA. With each multiple, I will start with a histogram describing how stocks are priced globally (with sub-sector specifics) and then provide country specific numbers in heat maps.

ת����ע��������

�������

������� ���ʵ���

���ʵ���

������Ѷ

������Ѷ ��ע����

��ע����